Most investors are not trying to outsmart markets or chase the next headline.

What they want is something far more practical: confidence that their money is working within a clear plan - one designed for the realities of life.

Markets rise and fall. Interest rates move. Unexpected expenses arise. And eventually, retirement arrives - a stage where volatility is no longer theoretical, but personal.

At True North Lifestyle, our investment philosophy is grounded in this reality.

We believe portfolios should be constructed to endure both favourable and challenging markets, while remaining aligned to your goals, your time horizon, and your tolerance for risk.

This means favouring clarity over unnecessary complexity, consistency over speculation, and long-term discipline over short-term noise.

Real lifestyle outcomes are not built through prediction. They are built through structure, alignment, and patience.

THE TRUE NORTH WAY

Great investing is rarely about predicting the next market move. It is about making consistently sound decisions over time - supported by structure, expertise, and governance.

At True North Lifestyle, every portfolio is built through the alignment of three essential elements.

First, your Certified Financial Planners - the advisers who understand your goals, your cash flow, your time horizon, and how you respond when markets become volatile. Investment strategy cannot be separated from the person it serves. Context matters.

Second, our Investment Committee. Portfolio decisions are debated, stress-tested, refined, and formally governed before implementation. This disciplined process is designed to prioritise evidence over instinct and structure over guesswork. Committee oversight reduces the risk of emotionally driven decisions at precisely the moments when discipline matters most.

Third, our external research and asset management partner, Resonant. Their team of professional investors and analysts monitor markets continuously, providing institutional-grade research, modelling, and asset allocation insight that supports our decision-making framework.

This structure exists for one reason: to ensure that your personal strategy is supported by a professional investment engine, with accountability embedded into every decision.

WHERE YOUR MONEY SITS -

AND WHY THAT MATTERS

One of the most important aspects of any investment strategy is understanding where your assets are actually held.

At True North Lifestyle, your investments are held on large, secure, and well-regulated retail investment and superannuation platforms. These platforms provide the custody, reporting, transaction execution, and administrative infrastructure that sit behind your portfolio. They operate within strict regulatory frameworks and are designed to safeguard client assets.

Importantly, funds do not “sit with” True North Lifestyle or with our research partner, Resonant. We do not take custody of your money, nor do we hold it directly.

You retain beneficial ownership of your investments at all times. Through your platform access, you can view, track, and verify your holdings independently. Your portfolio remains visible and transparent - not pooled into an opaque structure or inaccessible vehicle.

Our role is to advise on strategy, construct the portfolio, and oversee its management through a governed process. The assets themselves remain held within institutional platform infrastructure under your name and control.

TRANSPARENCY: YOU CAN

SEE WHAT YOU OWN

A common frustration in investing is not knowing exactly what sits inside a portfolio - or why changes were made.

Transparency at True North Lifestyle is not an afterthought. It is embedded into the structure of our managed portfolios.

You are able to see the underlying holdings that make up your portfolio. You can understand how it is positioned, how exposures are structured, and how those exposures align with your objectives. When adjustments are made by the Investment Committee, those changes are communicated clearly and reflected within your platform reporting.

Our portfolios are built using liquid, listed assets - including shares, exchange-traded funds (ETFs), and other listed market exposures. These instruments are market-priced and observable throughout the trading day.

This matters because valuation is not opaque or estimated behind closed doors. Pricing is anchored to live markets and independently verifiable.

Your portfolio is constructed from identifiable building blocks, not bundled into an inaccessible structure. You can see what you own, understand why you own it, and track how it evolves over time.

OUR INTELLECTUAL FRAMEWORK:

HOW WE BUILD PORTFOLIOS

What differentiates a durable investment strategy is not a product or a formula, but the framework beneath it.

At True North Lifestyle, portfolio construction begins with understanding the individual. Before any allocation is selected, we assess the factors that materially influence long-term outcomes: your time horizon, your need for income - whether immediate or future - your tolerance for volatility, your required rate of return (and what is realistically achievable), and your broader investment preferences. Strategy must be anchored in lived reality rather than assigned to a generic risk label.

We construct portfolios across seven distinct styles, ranging from high-growth accumulation strategies through to retirement income and capital stability solutions. Investors do not remain in a single life stage indefinitely, and portfolios should not assume they do. The breadth of our range allows for alignment today and adaptation as circumstances evolve.

A defining component of our framework is structured stress testing. Markets rarely repeat in identical form, but they do exhibit patterns under pressure. We model how portfolios would have behaved across major historical and hypothetical environments, including the Global Financial Crisis, pandemic-style market shocks, high-inflation and rapid rate-rise cycles, geopolitical and tariff pressures, and periods of bond market stress. This form of scenario analysis is widely used by institutional managers because it prepares decision-makers for adverse conditions, not merely favourable ones.

Portfolio construction also extends well beyond broad asset class labels. Diversification is not achieved simply by dividing capital between “shares and bonds”. We analyse the underlying composition of exposures — which types of shares are held (large or small capitalisation, growth or value, domestic or global), which investment styles are leading or lagging, where index exposure is efficient, and where active management may provide genuine value. We examine how each building block behaves under stress so that diversification is purposeful rather than superficial. The objective is not just to diversify, but to engineer resilience.

Finally, governance enables responsiveness without disorder. When markets shift, many investors either freeze or react impulsively. Our structure is designed to avoid both outcomes. The Investment Committee is able to convene, review evolving conditions, model the impact of potential adjustments, implement changes with discipline, and communicate those changes clearly. Responsiveness is embedded within a governed framework, ensuring decisions remain measured even during volatile periods.

Our objective is not to eliminate risk - that is neither realistic nor desirable. It is to understand risk, prepare for it, and manage it deliberately before it becomes disruptive.

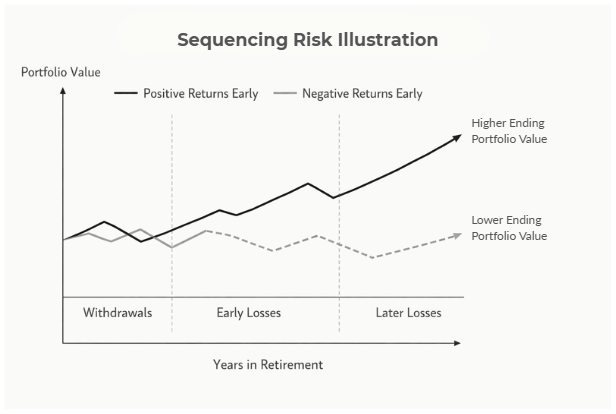

SEQUENCING RISK: WHY TIMING

MATTERS IN RETIREMENT

Most retirees focus on projected market returns. Far fewer consider the timing of those returns - yet timing can materially influence retirement outcomes.

During the accumulation phase, market downturns are uncomfortable but often manageable. Contributions continue, assets may be acquired at lower prices, and time supports recovery.

Retirement alters that equation.

Once income withdrawals begin, negative returns early in retirement can have a lasting impact. Capital may need to be drawn down during periods of market weakness, reducing the portfolio base available to participate in future recoveries.

.png)

This is sequencing risk. Two retirees may experience the same long-term average return, yet the individual who encounters adverse returns at the beginning of retirement may face significantly different outcomes from the one whose difficult years occur later.

For this reason, retirement portfolio design must consider more than expected returns. It must account for order of returns, withdrawal strategy, and capital preservation during the early years of income dependency.

At True North Lifestyle, portfolios are structured with this reality in mind. Diversification, defensive allocations, and disciplined income planning are incorporated to help manage risk during the stages of retirement when capital stability matters most.

Retirement sustainability is not determined solely by how much a portfolio earns, but by how those returns are experienced over time.

PORTFOLIOS DESIGNED FOR

LIFE STAGE, NOT JUST RISK SCORES

Investment portfolios should reflect more than a numerical risk tolerance result. They should reflect where you are in life, what you are trying to achieve, and how your financial priorities are evolving.

At True North Lifestyle, we maintain seven core managed portfolios. These can be implemented individually or blended together to achieve an appropriate balance of growth, income, and capital stability depending on your objectives.

For clients focused on long-term wealth building during the accumulation phase, our 75 Wealth Builder and 95 Wealth Builder portfolios are structured to prioritise capital appreciation. These strategies accept higher short-term volatility in pursuit of long-term growth potential.

For those approaching or in retirement, our 60 Income Generator and 80 Income Generator portfolios are designed with income sustainability in mind. They aim to support cash flow requirements while maintaining exposure to growth assets where appropriate, using broader diversification and income-oriented exposures.

For clients seeking targeted exposure to Australian equities, we offer Australian Equities Income and Australian Equities Core. These portfolios provide transparent access to listed Australian shares, with variations that either emphasise income generation or growth-oriented market participation.

Finally, our Enhanced Income portfolio serves as a defensive foundation. It prioritises capital stability and strong income characteristics. While it can stand alone, it is often used in combination with growth-oriented portfolios to help manage sequencing risk and provide stability during market downturns.

The strategic advantage is not in selecting a single portfolio label. It lies in constructing an appropriate blend that reflects your current life stage, and adjusting that blend as circumstances and objectives evolve.

If you would like to understand how these portfolios can be structured around your circumstances, our team can guide you through the process.

DESIGNED FOR INDIVIDUALS,

NOT THE “AVERAGE INVESTOR”

Many investment menus are constructed for scale. They are built to accommodate large groups of investors within predefined categories.

But retirement planning is rarely average. Cash flow needs differ. Risk tolerance shifts over time. Income requirements change. Market conditions evolve.

A portfolio framework should recognise this.

Active Oversight, Not Static Presets

Some investment options operate on a largely static model. Allocations are set at inception and may change infrequently, regardless of how markets or client circumstances evolve.

Our approach is governed by an Investment Committee that meets regularly to review economic conditions, asset valuations, portfolio positioning and risk exposures. Adjustments are debated, modelled and implemented through a structured process -not through automation or set-and-forget allocation bands.

This provides discipline without rigidity.

Transparency of Holdings

In many pooled investment options, investors see a fund name but have limited clarity on underlying exposures.

Our portfolios are structured so that clients can view the underlying holdings, monitor positioning, and understand the building blocks that drive performance. Changes are visible and communicated clearly.

Transparency enables informed confidence.

Flexible Portfolio Construction

Traditional investment menus often rely on broad labels such as “Growth,” “Balanced,” or “Conservative.” While these categories serve a purpose, they do not always reflect the complexity of an individual’s retirement timeline or income needs.

Our framework includes seven distinct portfolio strategies that can be implemented independently or blended together. This allows for more precise alignment to life stage, required return, volatility tolerance and income objectives.

The objective is not to fit you into a label - but to construct a portfolio around your circumstances.

Retirement-Aware Design

Many portfolios are built primarily with accumulation in mind. Retirement introduces additional variables: income sequencing, longevity risk, and capital preservation during withdrawal years.

Our portfolios are engineered with these realities considered. Defensive allocations, income-oriented exposures and sequencing-aware construction form part of the framework - not an afterthought.

Clear Communication

Investment adjustments should not occur in silence.

When portfolio changes are made, clients are informed of what changed, why it changed, and how it affects positioning. Ongoing communication is part of governance - not marketing.

This is not investing designed for brochures.

It is investing structured for real life - where goals, cash flow, markets and behaviour intersect.

If you would like to understand how this framework may apply to your situation, our team can guide you through a structured portfolio review.

HOW THIS WORKS IN PRACTICE

An investment philosophy has little value unless it translates into a disciplined, repeatable client experience.

This is how the framework operates in practice.

1. A Clear Plan Comes First

Before portfolio construction begins, we establish clarity around objectives.

This includes:

- The outcomes you are working toward

- The income required, and when it is required

- The timeframe over which capital must support you

- Your tolerance for volatility - both financially and behaviourally

The purpose is not to select a product. It is to design a financial strategy. Portfolio construction follows planning — not the other way around.

2. Portfolio Construction Aligned to the Plan

Once objectives, income requirements and risk parameters are defined, we construct a portfolio solution aligned to that framework.

For some clients, a single portfolio strategy is appropriate. For others, a blended allocation across multiple strategies better reflects their circumstances.

For example:

- A long-term accumulator may allocate primarily to a high-growth strategy.

- A client approaching retirement may blend income-generating and defensive portfolios to support sequencing management.

- A retiree drawing income may combine defensive assets with targeted equity exposure to balance stability and growth.

The portfolio is a tool. The financial plan determines how that tool is used.

3. Ongoing Governance and Oversight

Portfolio management is not static.

The Investment Committee meets regularly to:

- Review market conditions and asset valuations

- Monitor portfolio positioning and risk exposures

- Assess rebalancing requirements and tactical adjustments

- Evaluate defensive positioning when appropriate

Adjustments are considered within a structured governance framework. Decisions are documented, modelled and implemented with discipline rather than emotion.

4. Regular Review and Alignment

Markets change. Personal circumstances change. Portfolio positioning must reflect both.

Clients receive:

- Structured review meetings (at least annually, and more frequently where required)

- Communication when portfolio changes are implemented

- Updates regarding investment committee positioning

- Adjustments to portfolio blending as life stage evolves

This ensures the portfolio remains aligned not only to market conditions, but to your financial objectives.

An investment ethos is not marketing language. It is a process.

It is planning first.

Construction second.

Governance ongoing.

Communication consistent.

If you would like to understand how this framework may apply to your circumstances, we can discuss it in more detail.

UNDERSTANDING THE RIGHT PORTFOLIO FOR YOU

If you would like to explore how these managed portfolios may align with your objectives, timeframe and income requirements, we can review your position in more detail.

An Investment Strategy Session provides an opportunity to:

- Clarify your goals and retirement timeframe

- Assess your current portfolio structure

- Evaluate risk alignment and income sustainability

- Determine whether a single portfolio or blended approach is appropriate

The focus is not on selling a product. It is on establishing whether the framework outlined above suits your circumstances.

Kane Hansen

Founder, True North Lifestyle

A disciplined investment philosophy designed to help Australians navigate markets with clarity rather than complexity.

No obligation. Just a conversation about your strategy.

Important Information

The information provided on this page is general in nature and does not take into account your personal objectives, financial situation or needs.

Before making any investment decision, you should consider the appropriateness of the information in light of your own circumstances and refer to the relevant Product Disclosure Statements, Financial Services Guide and platform documentation.

Where appropriate, seek personalised financial advice.